Some people fear commitment but still crave loyalty. They want consistency, maybe even exclusivity—but without the legal entanglement. It sounds like a contradiction, but it's exactly the vibe in the final scene ofFour Weddings and a Funeral…….

Charles: Let me ask you one thing. Do you think - after we've dried off, after we've spent lots more time together - you might agree not to marry me? And do you think not being married to me might maybe be something you could consider doing for the rest of your life?

The same push and pull plays out between companies and individual workers. Under an “exclusive relationship” arrangement, companies are setting match preferences for loyal, top-tier talent invested in their mission, while individual workers are on the prowl for stable, well-paying gigs that offer security. When it comes to more of an “open relationship” setup, companies will “like” + “winky face” for the ability to scale quickly and cut costs, while individual workers swipe right for autonomy, freedom—and yes, the ability to work in their pajamas.

So let’s look at both sides of this modern commitment-phobia—the individual worker vis-a-vis the business—and what each party should actually consider before saying “I do.”

We’ll be approaching this topic from a US perspective; different countries handle employment law very differently. For example, in the US, at-will employment is the default employment relationship, and it means that an employer can terminate an employee at any time, for any reason (or no reason), with or without notice—as long as it’s not illegal. Likewise, an employee can quit at any time, for any reason, with or without notice.

For clarity: Throughout this piece, I refer to a business as the “employer” when it is engaging someone in an employment relationship, and as the “company” when it is engaging someone in a contractor relationship. I refer to the individual worker as either an “employee” or a “contractor,” depending on the nature of the relationship.

I. Employee v Contractor Differences

A) Employees:

When an employer hires an employee for a formal employment relationship (sometimes referred to as a W-2 employee after the IRS tax form W-2), it’s taking on a set of legal obligations and operational responsibilities in addition to paying a salary. That’s because employment—under US law—is a status, not just a relationship. Employees are protected by a range of labor laws that govern things like working conditions, harassment protections, and wrongful termination rights. In other words, with W-2 status comes both protection and structure for the employee, and responsibility for the employer.

Specifically, if someone is classified as a W-2 employee, the employer is legally required to:

Withhold and pay the employee’s income taxes, Social Security, and Medicare taxes (collectively known as “FICA” taxes)

Pay the employer-side portion of Social Security and Medicare (an additional 7.65%)

Provide a W-2 form at the end of the year for tax reporting

Often contribute to unemployment insurance and workers’ compensation funds (state-dependent - if no state workers’ comp fund, then employer must purchase private insurance)

Comply with wage and hour laws (like minimum wage and overtime rules)

Offer benefits like health insurance or retirement plans (sometimes applicable under federal law or state law - depends on local requirements, number of employees at the employer, etc.)

Follow anti-discrimination, leave, and labor protections (like FMLA, ADA, and Title VII)

B) Contractors:

By contrast, a contractor (aka freelancer, consultant, independent contractor or, referring to the IRS form tax form 1099, a 1099 contractor) is treated as an independent business. Being an independent contractor has its advantages: the contractor can set their own hours, take on multiple clients, more likely work remotely (many companies are calling employees back to the office or force quitting), and may be able to sidestep the internal politics of climbing the corporate ladder. Contractors may appear to take home more money up front than W-2 employees because no taxes are withheld from their pay—what they invoice is what they receive. However, that doesn’t mean the contractor’s total compensation is higher or equivalent. Why?

Contractors are fully responsible for their own financial and legal obligations. This includes paying 100% of their tax burden—the full 15.3% self-employment tax (both employee and employer portions of Social Security and Medicare)—plus regular income tax. With no automatic withholdings, they must file and pay quarterly estimated taxes. Miss a deadline, and the IRS adds penalties and interest.

Contractors also lack employee protections and benefits. They don’t receive:

Employer-sponsored health insurance

Access to employer-sponsored retirement accounts (and if lucky, employer contributions)

Pre-tax perks (e.g., commuting, childcare)

Certain protections under US employment law

That said, there are benefits to being a contractor. Contractors may be eligible for Section 199A “qualified business income” deductions, which can reduce taxable income by up to 20% (subject to carve-outs for certain service industries). This is a substantial tax benefit. Contractors can also deduct legitimate business expenses—such as home office costs, software subscriptions, and travel—which further narrows the financial gap with employees. When managed well, these tax advantages can meaningfully offset the additional burdens of self-employment.

The question is, from a cost perspective, is it worth it for the business or the individual worker financially to be a contractor?

II. How much does an employee cost an employer? Does the individual worker save money by being a contractor?

From a business’s perspective, acting as an employer by hiring an employee in California generally costs significantly more than just the employee's base salary. Employers are responsible for a range of payroll taxes—such as Social Security, Medicare, workers’ comp insurance, and federal and state unemployment insurance—and are often expected to provide a comprehensive benefits package that may include health, dental, vision, and life insurance. Using a contractor involves fewer financial obligations for the company, as contractors are responsible for their own taxes and benefits.

From the individual worker’s perspective, being a contractor means they must now cover self-employment taxes, purchase their own health insurance and other insurance or take the penalty, and forgo access to employer-sponsored benefits like guaranteed paid time off, disability coverage (varies but contractors could have disability through the state where they pay taxes), and retirement contributions. As a result, contractors would likely have to charge a considerably higher hourly or annual rate to achieve the same financial outcome as a full-time employee.

Let’s do some math to see how this works!

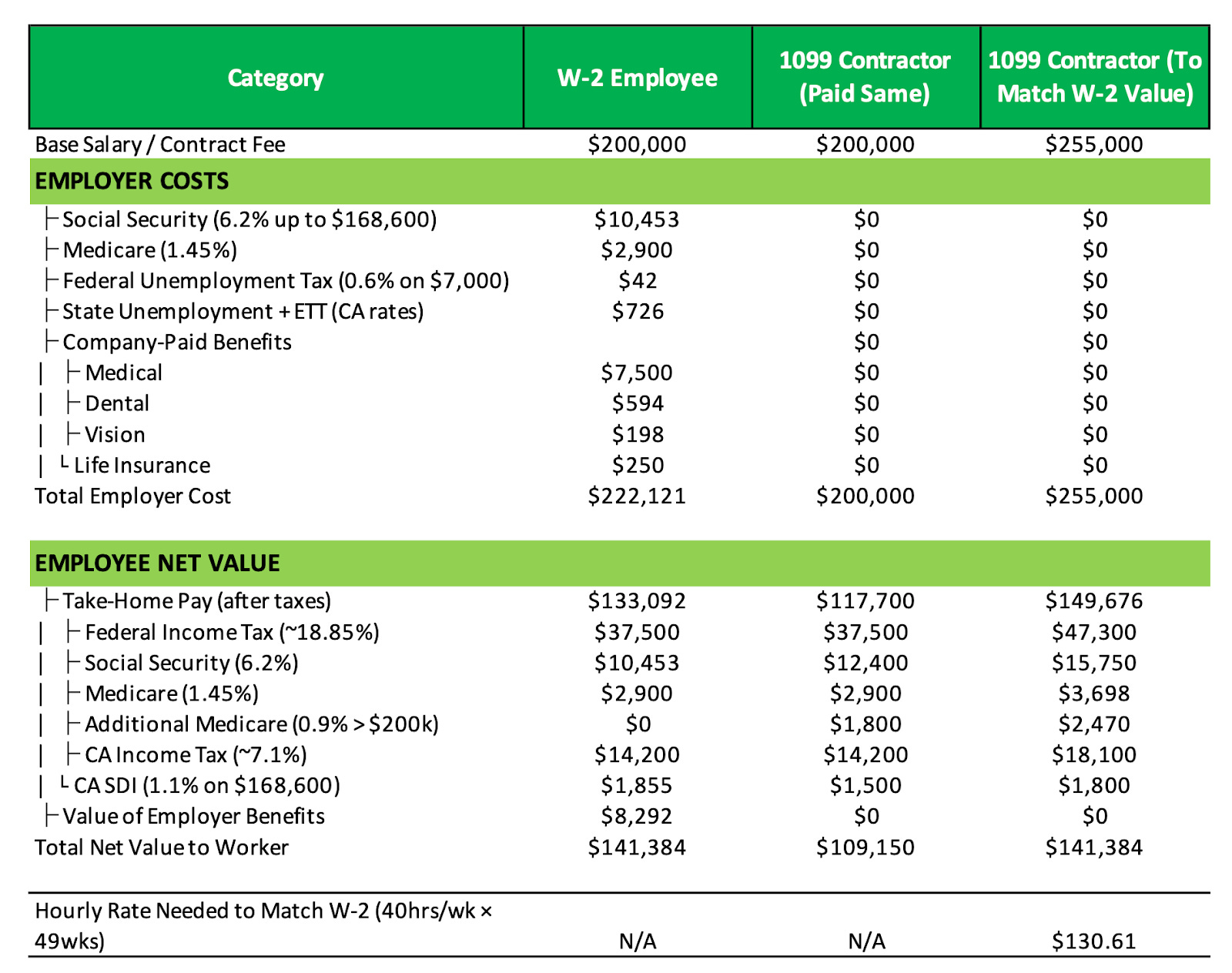

There are plenty of W-2 vs. 1099 calculators online, but for illustrative purposes, let’s use ChatGPT to model a single employee in California earning $200,000 annually, with the employer covering all healthcare costs and no 401(k) contributions for simplicity. I’ll assume as a contractor, the worker is doing 40 hours of work a week for 49 weeks of the year.

Note: This is a simplified example for illustrative purposes only. Actual taxes, benefits, and costs will vary depending on individual circumstances, deductions, and current regulations. This is not tax or legal advice. For full transparency, I’ll include the exact prompt used at the end of this article so you can try it yourself. Always consult a qualified tax advisor. The chart doesn’t include any potential deductions.

Takeaways:

For Businesses/Employers/Companies:

So you can see in the above chart, employers save money (around 20%) with contractors since there's no obligation to cover payroll taxes, health insurance, unemployment insurance, or other benefits. But that savings for employers comes at the expense of contractors. The contractor now covers the full cost of self-employment taxes, healthcare, insurance, and lacks access to paid leave or job protections. However, this cost-saving may come with tradeoffs, including less control over the worker, potential legal risks if the classification is incorrect, and the loss of team cohesion and institutional knowledge that can come with longer-term employees. We’ll dig into this a bit later For Individual Workers/Employees/Contractors:

Focusing on gross pay isn’t the full picture. A contractor may earn more upfront, but they keep significantly less. To match the take-home pay and benefits of a W-2 employee, a contractor would need to charge more to get to the same result. In this ChatGPT-run example, a contractor would need to charge $255,000 per year ($130.61 per hour) to get to the same net value as an employee making $200,000 per year for 40 hours a week for 49 weeks. On average, a contractor may have to charge 30-70% more than the equivalent base salary to get the same net take-home pay. Again, there are lots of factors that go into these numbers, but this should hopefully help to weigh the considerations.

While this shows a financial difference to the business and individual worker, this isn’t a full picture of the cost or benefit. There are other risks and costs to consider.

III. Misclassification Risk

Just because you call someone a contractor doesn’t mean the law will recognize them as such.

A) The cost of worker misclassification

Keeping a working relationship “complicated” has legal and financial consequences. As independent contracting grows (60 million Americans in 2022, with 90 million projected by 2028), regulators are paying close attention. In tech, contract roles exploded from 6% of postings in 2021 to 20% in 2022. And yet, an estimated 10% to 30% of U.S. employers are misclassifying workers, according to the National Employment Law Project.

The penalties to businesses are real and escalating. At the federal level, the Department of Labor can impose fines on businesses up to $1,000 per Fair Labor Standards Act (FLSA) violation, plus back wages (including unpaid overtime) and liquidated damages of 2x or 3x. Repeat violations can even lead to criminal charges.

Tax-wise, the costs add up fast. If a business misclassifies individual workers as contractors, the business may be required to pay a $50 fine for every unfiled W-2, 1.5% of the wages paid, 40% of the employee’s unpaid FICA taxes, and 100% of the employer’s share of unpaid FICA. If the misclassification is found to be intentional, the company could be liable for the full amount of unwithheld FICA and income taxes, plus reimbursement to the individual worker for Social Security and Medicare taxes they paid out of pocket.

States are piling on. In California, penalties range from $5,000 to $15,000 per violation—and up to $25,000 for repeat offenders. Add potential class action lawsuits from misclassified workers, and the exposure balloons.

Cases in point:

Uber paid $100 million to the state of New Jersey in 2022 after an audit revealed large-scale misclassification of drivers.

FedEx shelled out $228 million to settle claims with over 2,000 California drivers, some dating back over two decades.

B) How do you determine a person’s status as an employee v. contractor?

How individual workers are classified is a legal test: if the company controls how the work is done, sets schedules, integrates them into day-to-day workflows, or makes them economically dependent on that job—then legally, the worker may be an employee. Misclassification can trigger serious penalties: back taxes, back wages, fines, liability for unpaid benefits, and even class-action lawsuits.

So while using a contractor may feel flexible to the company, it’s only appropriate if the relationship is truly arms-length, preferably project-based and the service provided isn’t part of the core business. Even if both sides agree to the 1099, courts and agencies may dig into the true nature of the relationship.

TLDR: The label you choose doesn’t matter. It’s how the day-to-day relationship plays out that’s important. If they look, act, and smell like an employee, they probably are.

C) What can a business do to mitigate the financial and legal risk?

A business needs to be realistic about classification.

Before engaging a contractor, run a proper test using IRS and state-specific frameworks (IRS 20-factor test, California’s ABC test, etc.). The key element is often control.

Use a contractor agreement with clear deliverables and autonomy language.

Have the contractor invoice the company (plus points if it’s from an entity and not an individual).

Avoid giving contractors:

Company emails or equipment

Set hours or team lead oversight

Restrictions on taking on other clients.

IV. Contractors Dealing with Additional Costs of Being Contractors

Individual workers have additional costs and burdens if they are self-employed; a contractor can manage those costs by treating themselves like a business and planning ahead. They should talk to an accountant to game plan what is permitted and should be done to take full advantage of any tax savings. Specifically, a contractor could do the following:

Set aside a certain amount of every check for taxes.

Use bookkeeping software—or at the very least a spreadsheet—to track income and expenses.

Deduct everything they’re entitled to: home office, laptop, software subscriptions, phone and internet bills, and even a portion of health insurance.

Consider if it makes sense to pay quarterly taxes.

Given they get no employment perks, build their own benefits stack into their rate.

Contribute to a solo 401(k) or SEP IRA to lower their taxable income.

For more advanced planning, evaluate whether setting up an S-corp makes sense. Many contractors go this route to reduce self-employment taxes through “reasonable compensation” rules. Note, this comes with added administrative costs and complexity—another reason to have a solid CPA in your corner.

V. The Value of Having Employees or Being an Employee

For Employers: While a business may think it is saving money by using contractors, having an employee may save money in the long-term. Hiring full-time employees offers companies more than just reliable labor—it typically fosters long-term consistency and trust. Unlike contractors who may juggle multiple clients or roll off after short engagements, employees are generally more invested in the employer's success and culture and only need to be on-boarded once. That consistency may translate to:

Higher quality work: Employees tend to gain deeper knowledge of the employer’s systems, products, and workflows—making them potentailly more efficient and effective over time.

Institutional knowledge retention: Long-term employees accumulate context, history, and lessons learned that, and that “embedded wisdom” often helps teams avoid repeating past mistakes / speeds up decision-making.

Reduced retraining costs: Long-term team members retain institutional knowledge, meaning less time and money spent onboarding new people.

Stronger confidentiality: Employees are more likely to follow internal policies, protect proprietary information, and avoid conflicts of interest.

Cultural alignment: With ongoing exposure to company values, strategy, and leadership, employees often become better ambassadors and collaborators.

In short, while contractors can offer flexibility, employees offer continuity—and that can pay off in both performance and protection.

For Employees: Being an employee also offers advantages that go beyond steady pay. Employees benefit from:

Job stability and legal protections: Employees typically enjoy more consistent work, wage protections, and legal safeguards around termination, discrimination, and workplace safety.

Employer-sponsored benefits: Health insurance, retirement contributions, disability coverage, and paid time off can significantly enhance total compensation and provide peace of mind.

Professional development and advancement: Employees are more likely to receive structured training, mentorship, and promotion opportunities.

Sense of belonging: Being part of a team with a shared mission can foster stronger connections, purpose, and professional identity.

For many individual workers, the non-monetary benefits of being an employee—security, growth, and support—can be just as important as the paycheck.

V. Final Thoughts

The 1099 vs. W-2 question is less about titles and more about weighing costs, benefits, and risks. Not every relationship needs a marriage certificate. But some definitely need a prenup. Have awkward conversations up front and think about what’s right for you –whether you’re a business or an individual worker. Sometimes, it’s just more complicated to have an open relationship…

(control + F to replace bracketed info with other specifics]

“I am a [single] person in [California] earning [$200,000] per year as a W-2 employee. The company offers comprehensive benefits: health insurance (100% employer-paid for employee), dental and vision (99% paid), and life insurance (100% paid).

Please:

Create a fully itemized financial breakdown of what it costs the employer to hire me, including all payroll taxes and benefit contributions.

Break out each tax separately (Social Security, Medicare, FUTA, State Unemployment, etc.).

Break out each benefit separately (medical, dental, vision, life insurance).

Show my net take-home pay as a W-2 employee after federal, state, and employment taxes, with sub-line items for each tax.

Show the same scenario as a 1099 contractor earning [$200,000], with no benefits and including:

Self-employment taxes

Federal and state income taxes

The 199A/QBI deduction

Calculate the adjusted 1099 contractor income required to match the W-2 role’s total value (salary + benefits – taxes).

Calculate the hourly rate required for the contractor to match the W-2 value, assuming 40 hours per week for 49 weeks per year. Please ensure that the Contractor (To Match W-2 Value) column is fully calculated by solving for the contractor gross income required to equal the W-2 net value, rather than leaving placeholders.

Output a professional Excel table in HR-style format with three scenarios as columns:

W-2 Employee

1099 Contractor (Paid Same)

1099 Contractor (To Match W-2 Value)

Export to an Excel

Excel Formatting Requirements:

1. Top Header Row

Dark green background with bold white text.

Columns:

Category (line items)

W-2 Employee

1099 Contractor (Paid Same)

1099 Contractor (To Match W-2 Value)

This creates three comparison scenarios.

Below the Top Header Row, put a row with “Base Salary/Contract Fee” on the first cell. Then, put the amount I stated above in the next few cells for the pay amount. In the 4th cell, calculate the gross amount you’d have to make as a contractor to walk away with the same net value as an employee.

2. Employer Costs Section

Has a lighter green section header row labeled EMPLOYER COSTS.

Line items underneath are indented for clarity:

Social Security (with rate & wage cap noted)

Medicare (with rate noted)

Federal Unemployment (FUTA)

State Unemployment (SUTA/ETT)

Company-Paid Benefits: Medical, Dental, Vision, Life Insurance

Ends with an italics subtotal row: Total Employer Cost.

Put an empty row between this and next section.

3. Employee Net Value Section

Another lighter green section header row labeled EMPLOYEE NET VALUE.

Breaks out employee’s take-home pay and taxes, with sub-items indented:

Take-Home Pay (after taxes)

Federal Income Tax

Social Security

Medicare

Additional Medicare (if applicable)

[CA Income Tax]

[CA SDI]

Also includes Value of Employer Benefits as a separate line item.

Ends with an italics subtotal row: Total Net Value to Worker.

For 1099 contractor columns, include a full tax breakdown mirroring the W-2 format:

Show “Take-Home Pay (after taxes)” as gross income minus all of these.

4. Bottom Summary Row

A final row separated by top and bottom borders.

Bold text: Hourly Rate Needed to Match W-2 (40hrs/wk × 49wks). Put a line on the top and the bottom of this row.

Only the “Contractor (To Match W-2 Value)” column shows a figure (e.g., $130.61).

5. Formatting Features

Color coding: dark green (top headers), light green (section headers).

Indentation for sub-items.

Bold totals for emphasis.

Currency formatting ($#,##0) for all monetary values.

Text left-aligned, numbers right-aligned for readability.

Cells that have a value of zero, put “$0”

{ChatGPT can be finicky so you may need to play with it a bit to make sure it generates everything properly. We can’t guarantee it will output the exact same way but hopefully it helps you get a foundation for a prompt. Again, not advice.}

Images:All original images are AI-generated with using a combination of Dall-E, Firefly, DreamStudio and Pixlr.

Disclaimer: This post is for general information purposes only. It does not constitute legal advice. This post reflects the current opinions of the author(s) and are for educational purposes only. The opinions reflected herein are subject to change without being updated.