LawBurst: U.S. Uniform Commercial Code Gets an Upgrade for Digital Assets

Understanding American commercial law, secured transactions, and the 2022 amendments to the Uniform Commercial Code for crypto

[What is a LawBurst? A short, information-packed legal article that’s a roughly written breakdown of something interesting.

I found myself re-reading and re-listening to some great legal minds out there about Article 12 of the Uniform Commercial Code (shout out to Drew Hinkes, Carla Reyes and Andrea Tosato). Forget the steam engine, the printing press or the iPhone -- legal innovation is super cool. Enjoy!]

[Created by Benjamin Franklin in 1754, the “Join or Die” Flag urged colonial unity and warned of the dangers of disunity during the French and Indian War. During the American Revolutionary War, it became a symbol for resistance to British rule. We’ll see why apropos for how the Uniform Commercial Code works.]

Background: How Commercial Law Works in the US

In contrast to many other countries, the United States does not operate under a centralized system of federal commercial laws. To address this and foster consistency throughout the country, the Uniform Commercial Code (UCC) was introduced in 1952. This groundbreaking initiative, undertaken collaboratively by the Uniform Law Commission (ULC) and the American Law Institute (ALI), established a standard set of commercial law that could be applied anywhere in the US enhancing the predictability and efficiency of commercial transactions.

How does it work? The UCC is proposed, model legal language on which each US state can base its commercial laws (i.e. it’s suggested text for legislators to adopt and implement in their respective states). Unless a state decides to copy and paste the UCC text into its laws, it will have no legal effect. The state legislature must pass it into law. Often, states will adopt pretty much word for word the model language, but that’s not always the case. In practice, every state and most independent jurisdictions within the U.S. have adopted most, if not all, of the UCC.

Who writes it? Legal experts (judges, legislators and law professors) in collaboration with the American Law Institute draft the UCC text, and over the years, they’ll come up with new language (either as an update to prior text or as a whole new subject matter) so that the law evolves with the times.

What does it cover? Over the years the UCC has come to address various topics in commercial law, including sales and leases, negotiable instruments, bank deposits and collections, letters of credit, bulk sales, documents of title, investment securities, and secured transactions. From time to time, the UCC model language is amended or augmented. In 2022, the latest amendments introduced coverage for secured transactions of digital assets. Let’s double click on this topic.

What Is a Secured Transaction?

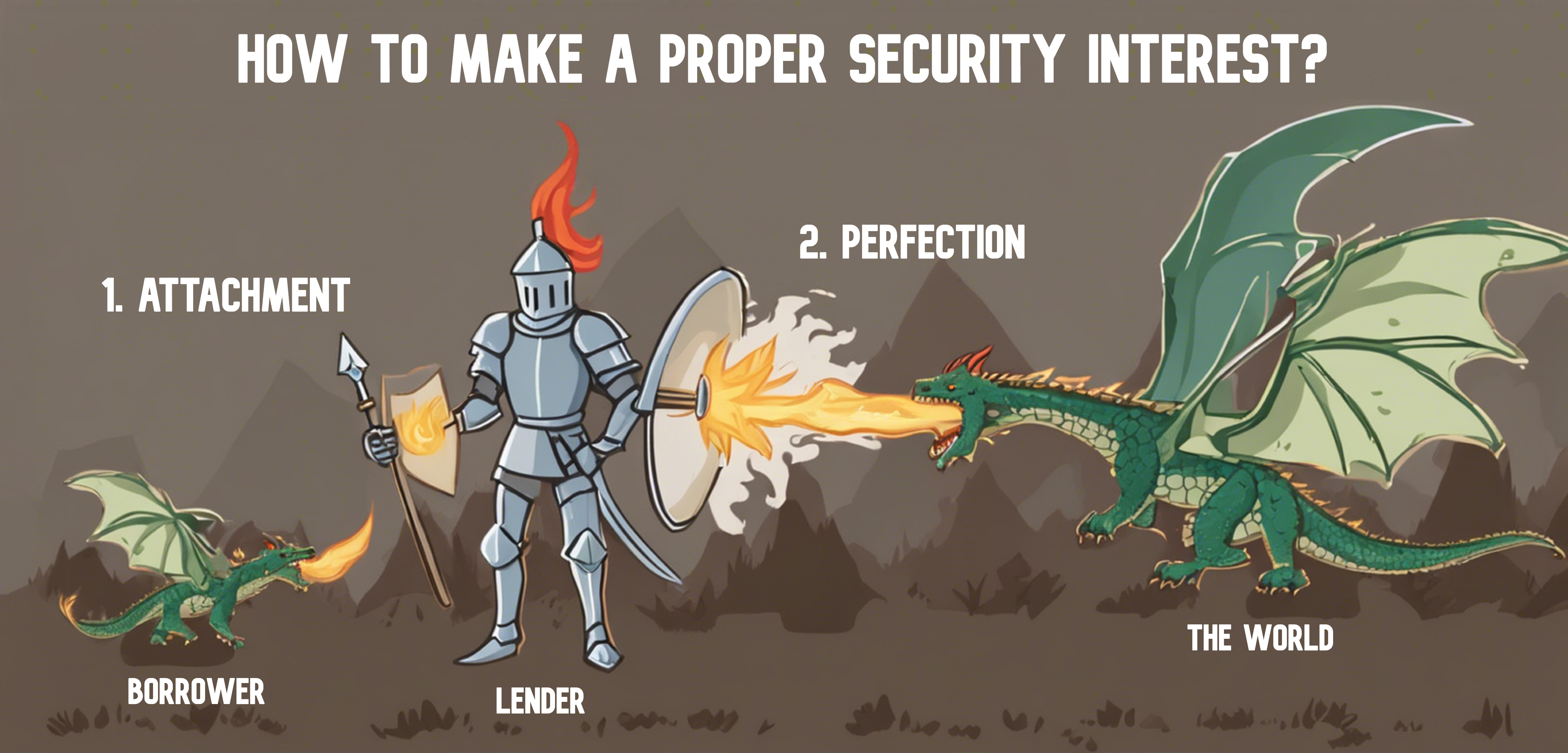

A secured transaction is a loan in which the borrower gives an asset (collateral), which the lender can take in case the borrower can’t pay back the loan (defaults on the loan). The collateral is a security interest that gives the lender a Plan B (seize the collateral) in case the borrower defaults.

Article 9 of the UCC governs secured transactions and lays out the mechanics for how a secured transaction properly works. In order to have a 100%, no take backs security interest in the collateral for a loan, a security interest must both (1) attach and (2) be perfected. You can think about attachment and perfection as the legal shield against (i) the borrower and (ii) the world, respectively.

Attachment: For a security interest to attach, the lender needs 3 things to happen: (i) the lender must give something of value for that security interest (like money), (ii) the borrower needs to have rights to the collateral or the power to transfer it to another party and (iii) the borrower must sign a written, security agreement. That secures your rights to collateral -- at the borrower level.

Perfection: The proper method of perfecting a security interest depends on the type of asset being used as collateral. Potential methods include (i) filing a financing statement (known as a UCC-1 form) with a filing office, (ii) possessing the collateral, (iii) having control of the collateral, or (iv) happening automatically. As an example, cash can only be perfected by possession, and goods can be perfected either by possession or filing a financing statement. Perfecting an asset correctly, secures priority over an asset ensuring the lender’s claim supersedes all others. Here’s an example of a financing statement for Texas.

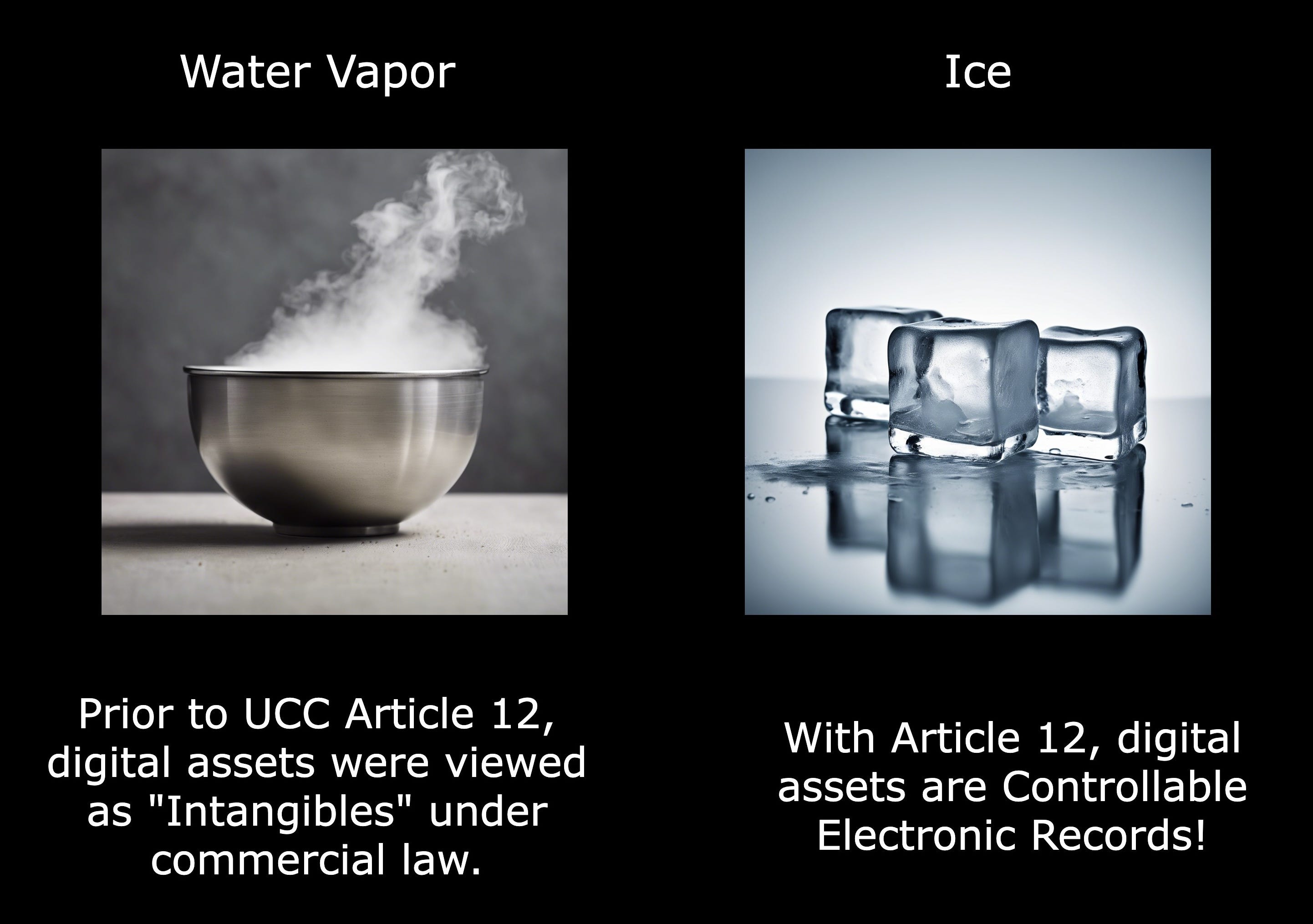

What type of asset was a cryptocurrency? There was a catchall category of assets known as “general intangibles” under UCC Article 9, which was meant to include an asset that couldn’t be physically controlled or possessed (ex. accounts receivable, proceeds, patents, trademarks, goodwill, etc.). Security interests in which intangibles were used as collateral could only be perfected by filing a financing statement with the filing office. Because cryptocurrencies were deemed “general intangibles,” filing was the only way to perfect the security interest in a token. However, the preferred method for perfecting security interests with crypto as collateral changed with the 2022 updates to the UCC, which revised the existing Article 9 and introduced a new Article 12.

UCC Article 12 (Controllable Electronic Records)

Article 12 of the UCC provides a legal regime for digital assets by introducing a new category of assets known as controllable electronic records (CER), which is a “record stored in an electronic medium that can be subjected to control under [the article].” To be clear, these model rules have nothing to do with whether crypto is a security or a commodity, tax rules, sanctions laws, or anything else like that. Its purpose is to provide standardization of commercial transactions of digital assets across the country. Most cryptocurrencies, tokens, stablecoins, and NFTs would likely be classified as CERs.

How do the 2022 updates to the UCC fix the perfection issue with crypto? Instead of having to file a UCC-1 statement, control is the preferred method of perfecting a secured interest in a CER. Control exists when a holder:

can access and enjoy nearly all of the benefits derived from the CER;

possesses the “exclusive power” to prevent others from enjoying “substantially all the benefit” of the CER; and

holds the sole right to transfer control over the CER. It is important to note that control is not revoked when shared consensually or facilitated by technology, such as by using a multi-sig transaction.

So now, under the new UCC model rules, you can perfect a secured interest through control. You also have the option to identify yourself as the person having control either by name, cryptographic key or account number.

What else does Article 12 do? Great question! Under Article 12, CERs can have many of the attributes of negotiable instruments. Negotiability refers to a feature of financial instruments that allows them to be transferred without any competing claims. Before the updates, anyone who acquired a token from another person (known as an onward transferee) could never truly be sure they owned said token free and clear unless they checked for a filed financing statement. But with the new amendments, CERs have increased transferability. Let’s give two common property law examples: the “shelter rule” and the “take free rule.”

Under the shelter rule, purchasers of a CER obtain whatever rights to the property the original transferor had or had the power to transfer.

Under the take free rule, a purchaser who takes control of a CER for value, in good faith, and without notice of a prior claim to the property (a qualifying purchaser) obtains the interest in the CER free of any restrictions of ownership (encumbrances).

The design of cryptocurrencies and the expectation of its users is for crypto to trade freely, and the default rules for intangibles just didn’t work in practice. Ingeniously, the UCC amendments uphold the decentralized ethos of cryptocurrencies, ensure secured lenders can legally operate as the rest of the industry, and safeguard the unencumbered transferability of crypto. In other words, the UCC has caught up to the technology.

Why doesn’t filing a financing statement work for crypto? People treat cryptocurrencies as bearer-like assets that free flow between parties. A bearer asset is one that can be freely traded and whomever is in possession owns the asset (like gold or cash). In other words, you don’t need to record ownership or have paperwork to prove ownership; possession indicates ownership. In practice, people in crypto extending loans with tokens as collateral don’t tend to perfect their security interest by submitting a financing statement. Web3 degens like to say that “code is law” meaning that you can rely on the code to automatically carry out the rules of the system. Digital ecosystems have designed their own practices and sets of rules to define the distribution of powers within a system without needing to rely on contractual enforcement.

Why is it so important to properly perfect a security interest in crypto collateral? Although there may be a desire for crypto systems to operate independently from the boring, grown-up world, failing to update laws to accommodate new technologies risks adverse outcomes.

One example, crypto secured lenders run the risk of being unperfected secured lenders if they don’t properly perfect collateral and the borrower were to default on a loan. If a second lender took a security interest in the same collateral as the first lender and s/he properly perfected it, the second lender could have a first priority right to the same collateral. For the lender who holds a token but hasn't filed a financing statement (trying to rely on possession as the method of perfection), s/he would be considered an unperfected secured lender. That means you lose the collateral to the party who properly perfected, or if the borrower went bankrupt, you’d have to deal with the bankruptcy process.

Second example, improperly perfected tokens would lead to an onward transferee receiving encumbered or partial property rights without the take free rule and shelter rule described above. As a result, tokens would be less transferable and ownership or rights to the tokens could be fragmented.

Conclusion: Let’s Put the Uniform in “Uniformity”

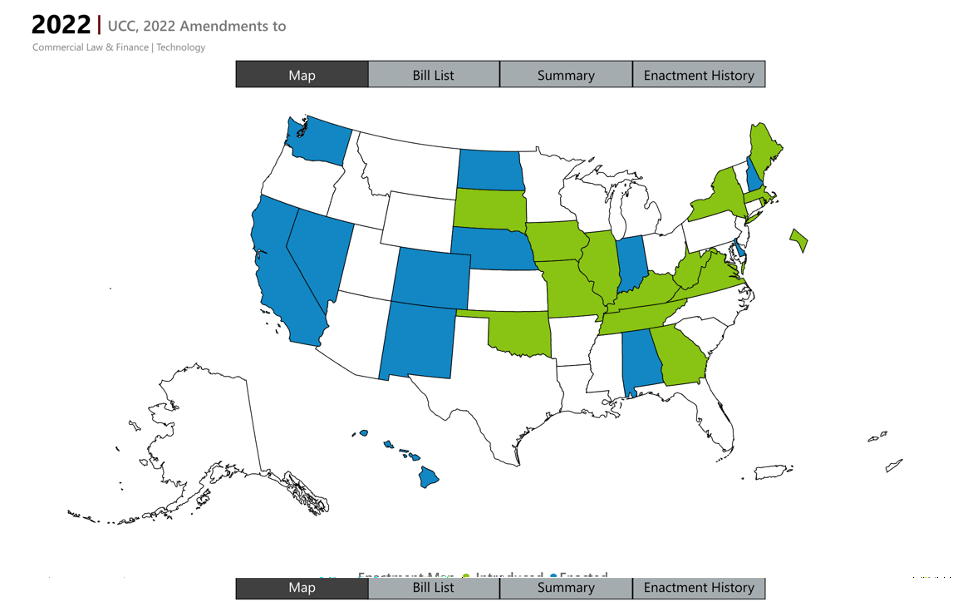

[From the UCC: As of February 2024, above shows the states that introduced or enacted the UCC amendments (including Article 12 amendments.]

As of February 2024, the 2022 UCC amendments have been adopted by 12 states and introduced in 15 others. However, some states like Florida and South Dakota have opted out because they also address central bank digital currencies (CBDCs). Under the model rules, CBDCs are not CERs but have been classified as “electric money,” which is defined as a “medium of exchange that is currently authorized or adopted by a domestic or foreign government.”

According to law professors Carla Reyes and Andrea Tosato, such actions are politicizations of what should normally be non-controversial updates to the commercial code and indicate a fundamental misunderstanding of commercial law. Not providing clear rules around digital assets just hurts crypto users in those states. Please read more about that here and here.

[Spread the word to your local governments!]

Just as vaccines are most effective when administered widely to establish herd immunity, the efficacy of the UCC’s model rules is maximized when adopted by all 50 states, creating a harmonized framework of commercial law throughout the nation. It streamlines transactions, reduces costs, eases dealings, simplifies paperwork, reduces uncertainty, and brings order to a previously chaotic system. Until the 2022 amendments pass across the country, we’ll have to deal with a patchwork of differing rules.

Resources:

Uniform Law Commission, UCC, 2022 Amendments to, https://www.uniformlaws.org/committees/community-home?communitykey=1457c422-ddb7-40b0-8c76-39a1991651ac

Uniform Law Commission, Uniform Commercial Code, https://www.uniformlaws.org/acts/ucc

Latham & Watkins LLP, The UCC Gets a Digital Asset Refresh, August 10, 2022, https://www.jdsupra.com/legalnews/the-ucc-gets-a-digital-asset-refresh-2857883/

American Bar Association, Crypto, Part III: Securing Interests in Digital Assets—The Proposed UCC Article 12, Steven Aquino, May 23, 2023, https://www.americanbar.org/groups/litigation/resources/newsletters/corporate-counsel/crypto-part-3-securing-interests-digital-assets-the-proposed-ucc-article-12/

Why Crypto Needs UCC Article 12, Andrew Hinkes, October 28, 2022, https://www.coindesk.com/layer2/2022/10/28/why-crypto-needs-ucc-article-12/

Florida’s DeSantis Waging Toothless Campaign Against Digital Dollars, Lawyers Say, Jesse Hamilton, May 17, 2023, https://www.coindesk.com/policy/2023/05/17/floridas-desantis-waging-toothless-campaign-against-digital-dollars-lawyers-say/

National Constitution Center, The Story Behind The Join Or Die Snake Cartoon, May 9, 2023, https://constitutioncenter.org/blog/the-story-behind-the-join-or-die-snake-cartoon

DePaul University Business and Commercial Law Journal, Description of the Collateral Under Revised Article 9, Cynthia Grant, Winter 2006, https://via.library.depaul.edu/cgi/viewcontent.cgi?referer=&httpsredir=1&article=1191&context=bclj

Duke Law, Uniform Commercial Code, https://law.duke.edu/lib/research-guides/ucc

Northwestern University Law Review, Emerging Technology’s Unfamiliarity With Commercial Law, Carla L. Reyes, 2024, https://scholarlycommons.law.northwestern.edu/cgi/viewcontent.cgi?article=1340&context=nulr_online

Crypto’s Future Is at Stake in a Dispute Over Commercial Law’s Definition of Money, Carla L. Reyes and Andrea Tosato, April 7, 2023, https://www.barrons.com/articles/crypto-commercial-laws-definition-of-money-5fbd8fe4

Instructions for UCC Financing Statement (Form UCC1) in Texas, https://www.sos.state.tx.us/ucc/forms/UCC1.pdf

Code is Law?! (#codeslaw), CBER Forum on Youtube, Youtube Link

The Law of Code Podcast, Episode 85, UCC Article 12 Amendments with Drew Hinkes and Andrea Tosato, December 2022, Spotify Link

The Encrypted Economy, Episode 72, How Do You Create a Security Interest in a Digital Asset? Professor Carla Reyes, Southern Methodist University School of Law, https://theencryptedeconomy.com/podcast/how-do-you-create-a-security-interest-in-a-digital-asset-professor-carla-reyes-southern-methodist-university-school-of-law-e72/

World Health Organization, How Do Vaccines Work?, December 8, 2020, https://www.who.int/news-room/feature-stories/detail/how-do-vaccines-work

Knight Security Interest image partially generated by DreamStudio

Water Vapor/Ice image partially generated from DreamStudio

Disclaimer: This post is for general information purposes only. It does not constitute legal advice. This post reflects the current opinions of the author(s). The opinions reflected herein are subject to change without being updated.