Congratulations! You’ve just received a job offer from a startup—an exciting milestone full of possibility and new beginnings. While offer letters usually cover a range of details—like your role, manager, location, salary, benefits, and bonus—the equity piece is often the most complex. It’s one of the most important aspects to understand, as it can have a significant impact on your long-term financial future. That’s what we’ll focus on here.

You know how, when you have a weird mole on your back, you ask your doctor friend to take a look? Think of this as the legal equivalent—here to help you make sense of the fine print in your offer. No billable hours, just unsolicited (but hopefully helpful) opinions.

When you join a startup, your compensation will likely be a mix of cash and equity. It’s important to negotiate the right balance between these two components based on your financial needs and the perceived value of the equity.

If you believe the startup’s equity has significant growth potential, you might want to push for a higher equity percentage. However, if you’re unsure about the company’s future or prefer financial stability, it may be prudent to negotiate for more cash.

B. Types of Equity Under a Stock Plan

Equity in a startup can come in several forms: stock options, restricted stock units, or direct stock awards.

Stock options give you the right to purchase a company’s common stock at a set price (the strike price) during a specified period of time.

Restricted Stock Units (RSUs) are promises to give you stock, or the economics based on the underlying stock value, in the future, which are often tied to performance or time-based vesting.

Direct stock awards or sales are when you receive stock outright or have the opportunity to buy it (typically at a discount). Unlike options, RSUs and direct awards usually come with immediate tax implications.

We’re focusing on options here because startups prefer them. Why? They align employee incentives with company growth, are easier to manage than other equity types, and offer tax advantages for both sides. Options also simplify things when employees leave—unvested options automatically return to the pool. Unlike stock grants, they defer taxes until exercised and don’t require upfront payment. Plus, they let employees buy shares at a discount if the company’s value increases.

Note, options are appropriate for earlier stage startups. A later-stage company may shift from using options as the default form of employee compensation to RSUs. Also, earlier stage startups tend to use their law firm’s forms without minimal changes. Later on, you’ll see more bespoke stock plans.

C. Stock Options: The Basics

Here are some essential concepts to understand and focus on as you try to make sense of your equity package:

Number of Shares/Strike Price: Your offer letter should specify how many shares the options entitle you to purchase. To understand what that means for you financially, you’ll need to know the strike price (aka exercise price) for those shares. The strike price is the price at which an employee can buy company common stock when exercising their options, typically set at the stock's fair market value (FMV) on the grant date.

Calculating the Total Exercise Price: The total exercise price of your options is equal to the number of shares under the grant times the strike price. For example, if the company offers you an option to purchase 3,000 shares at $1.00 per share, that means that you have to pay $3,000 (3,000 x $1) to exercise the options (note that you can elect to partially exercise any portion of the options once they are vested). The idea is that in the future, assuming the value of the company has gone up, you are buying your shares at a discount (i.e. the strike price).

409A Valuation: A 409A valuation is an independent appraisal used to determine the FMV of a private company's common stock. The FMV is used to set the exercise price of stock options, ensure compliance with IRS regulations, and avoid potential tax penalties.Under the prior example, if the 409A Valuation is $1.00 per share of common stock, then the FMV of the shares is $3,000 at the time of the grant.

Bringing these concepts together, at the time of the option grant, the exercise or strike price should equal the 409A valuation on a per share basis. Companies typically use the 409A to set the FMV of option grants. If a company offers you an option with a strike price below FMV, that’s a red flag and can lead to high tax penalties.

Authorized v. Outstanding Shares. Authorized shares are the maximum number of shares a company can legally issue, as set by its certificate of incorporation — but they don’t reflect actual ownership. It’s just a cap on how many shares a company may issue. Outstanding shares are the shares that have been issued and are currently held by shareholders like founders, employees, and investors. To calculate your actual ownership, use the number of outstanding shares as your baseline.

Fully-Diluted Shares: The fully-diluted shares refer to the total number of shares that would be outstanding if all convertible securities, such as stock options, warrants, and convertible bonds, were exercised or converted into common stock. This represents the maximum potential share count and is often used to assess more holistic ownership percentages and company valuation. Because companies all have different valuations, understanding your percentage of the fully-diluted shares is a digestible way to compare apples and oranges. More on this later!

Vesting Schedule: This is the timeline over which you earn your equity. Companies use vesting to encourage you to stay with them and contribute to the company’s success over the course of years. Vesting typically occurs on a time-based schedule, which is usually over four years with a one-year “cliff”, meaning you’ll earn 25% of your equity after one year and then continue to vest monthly, quarterly, or yearly over the remaining 3 years. Sometimes you see vesting over 5 years, and you may also see vesting that does not include a cliff. Once options are vested, the employee can exercise them, meaning they can purchase the underlying shares at the strike price. Vesting usually starts on your first day of work, so you’ll want to confirm the date your option starts vesting (known as the “vesting commencement date”). If you are no longer providing services to a company, any unvested portion of your options is usually automatically returned to the option pool.

Acceleration: If you have the clout, you may be able to negotiate vesting acceleration, which accelerates the vesting of the equity upon certain triggering events, such as the sale of the company or involuntary termination. Single-triggeracceleration (STA) occurs upon the sale of the company or an involuntary termination, leading to the immediate vesting of some or all equity. Double-trigger acceleration (DTA) occurs when an involuntary termination without cause follows the sale of the company, leading to accelerated vesting. Acceleration is difficult to negotiate as an employee—especially single-trigger acceleration, which is relatively rare. However, it’s worth asking if a company offers any acceleration. For founders, acceleration is a way to protect yourself. FWIW, many investors are fine with DTA but may balk at STA.

Early Exercise Option: Some companies allow you to exercise your stock options early, meaning you can buy both vested and unvested shares. Unvested stock remains subject to vesting. Note that early exercising requires upfront payment, and you will have to pay ordinary income taxes on the spread between the exercise price and the then-current FMV. However, early exercise offers tax benefits. First, you get the benefit of being taxed only on the spread between exercise price and FMV at exercise, as opposed to the stock’s value in the future. Also, if you hold the shares for at least one year, the proceeds from their sale will qualify for long-term capital gains tax rate. However, you will need to file an 83(b) election with the IRS (VERY IMPORTANT!) upon exercising an unvested option. Whether vested or unvested, once you exercise your options, you become a stockholder and can vote your shares.

In addition to the out-of-pocket costs of early exercising, there are additional risks: losing the money if the company fails or if the shares lose value, owing taxes like alternative minimum tax (AMT) (a backup tax to prevent high earners from overusing deductions) or income tax, illiquidity until an IPO or limited secondary transactions, and the possibility of a company buyback of unvested shares at a potentially lower value if you leave. I recommend seeking advice from your tax professional on whether early exercising makes sense for you.

Pro Tip: There are companies like SecFi that offer tools for scenario modeling, tax planning, and financing options (i.e. loans for option exercising). These are worth looking into to assess your options.

Now that we have a grasp of some of the basic terms, let’s talk about the Stock Plan and what to watch out for in the documentation.

D. Read the Stock Plan!!!

The stock plan (sometimes colloquially referred to as the option pool or stock pool) sets the overall rules and framework for the company's equity compensation, while the individual stock option agreement details the specific terms of the stock options granted to an individual employee within that framework.

In this section, all snippets will be from the 2020 Neurospace stock plan

Make sure you request a copy of and thoroughly review the company’s stock plan. It outlines crucial details like option expiration dates, rights of first refusal, and transfer restrictions. You usually won’t be able to get a copy until you onboard, but you can still ask about some of the below key terms:

Expiration: So long as you are still working for or engaged with the company, options typically expire 10 years from the date of grant.

BUT, if your service ends, options oftentimes expire 3 months after termination (or 6 months in the case of disability). Sometimes, you’ll see longer expiration periods so don’t assume anything (read the plan!). After you leave, you’ll need to make a quick decision if you want to exercise the options.

Since this can mean an all or nothing decision soon after you leave the company, you can try to negotiate for a longer window or use a company like SecFi to trade some of the potential upside for not losing the option entirely by not exercising.

Transfer Restrictions/Liquidity: Often, there are restrictions on transferring common stock. Even though you own shares, you may not be able to sell your shares without the company’s approval. This is important because you want to know if you can sell your shares before an IPO or sell on a secondary market. You would need to check the stock plan and also the company’s bylaws.

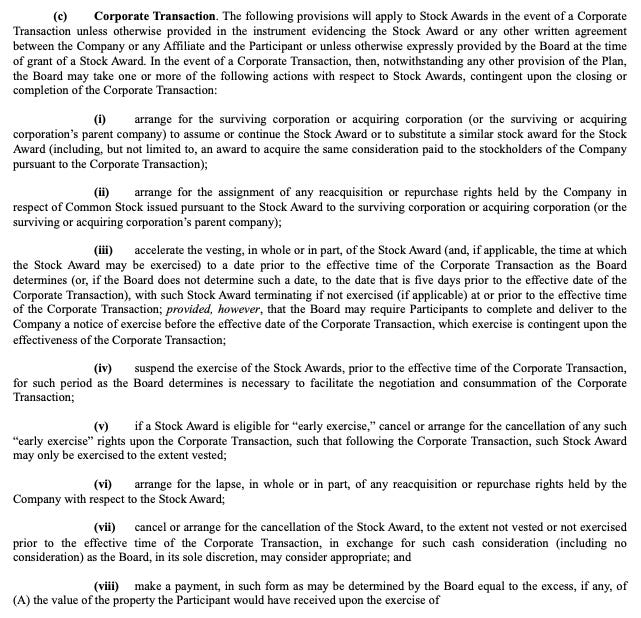

Change of Control: What happens to your unvested stock options if the company gets acquired? In the event of a merger or acquisition, options and shares under the plan will be treated as specified in the transaction agreement, which may include continuation, assumption, substitution, or cancellation with or without payment. Per this catchall, you could get nothing! Stay alert on the job—keep an eye out, listen closely, and try to sense any signs of a potential change of control, like shifts in leadership, strategy, or unusual activity behind the scenes.

Here are some examples of unusual additions to a stock plan you’ll want to keep an eye out for:

Payment Method: The company may block loans against the options or shares.

Fee Per Transfer: The company may require a fee per transfer.

Clawback Provisions: If you violate a non-compete or non-solicit agreement or get fired for cause, the company can take back shares or the proceeds you make from selling the shares.

Holding Period Requirements: The company may require you to keep a certain percentage of vested shares for a while, even after fully vested.

Repurchase Rights: The company might be able to buy back shares at a set price, which could limit your ability to sell them.

E. How to Value Your Options

Now that you’ve reviewed the key terms in your stock plan, let’s dive into how to actually value your options. This section will walk you through what to ask for, what to look for in public documents, and how to make rough estimates when information is limited.

1) Calculate the paper value of your option

To calculate the value of your option grant, multiply the FMV of the common stock by the total number of shares granted. Where do you find the FMV? Two ways: the ideal way and the “make it work” way.

Ideal Way: Ask the company for their 409A valuation and when it was calculated.

If the company can’t tell you the 409A valuation and when it was calculated, that’s a red flag that they either don’t know what they are doing or they are being secretive. If you can’t get the official valuation from the company, there are ways to do some back of the envelope calculations (i.e. very rough estimates) on your own.

Alternative (Make it Work): Use the company’s certificate of incorporation (COI) to calculate the value of the common stock.

A COI is a public document that generally anyone can pull from the US state the company is incorporated in (usually Delaware). So, if the company doesn’t want to give you the COI, you are more than free to request it yourself directly from the state of incorporation. Once in hand, here’s what you can do yourself:

Find the Last Price of their Financing Round: The COI will tell you the price per share (PPS) of preferred stock (usually called the “original issue price”) and the number of authorized shares for each class and series. Look at the very last series of the preferred stock’s original issue price (ex. if their last round was a Series C, then look at the Series C original issue price).

Calculate the Value: The current 409A value is often around 20%-30% of the price for a Series Seed Preferred Stock after the Seed round. That goes up over time and gets closer to 40% after a Series C round and can be an even greater percentage if the Company has a lot of secondary activity. So, if the last round the company did was a Series Seed round and the Series Seed Preferred Stock price was $1.00, the company’s common stock will probably be valued somewhere between $0.20 to $0.30 per share. Caveat that the value of the common stock should, in theory, go up over time—so if it’s been a few years after a round and the company has not raised further funds, the value of the common stock may be out of those ranges.

Example: let’s look at Uniswap’s COI from 2022:

Looking at Uniswap’s 2022 COI, they had done 2 preferred rounds. The PPS of the Series A Preferred Stock was $2.35617 so it’s likely that the 409A valuation after the round was around $0.47, or 20% of the PPS. Again, not a precise calculation, but a rough, rough estimate. If you can, always get that official 409A valuation.

2. Figure out where you fall in the liquidation stack

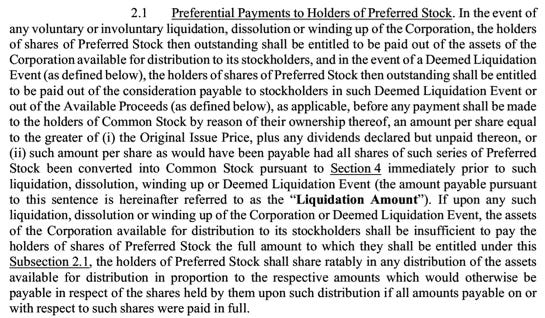

Your option grant might look valuable on paper—but that value only matters if there’s enough money following a liquidation event to pay out to shareholders. That’s why it's important to understand where you sit in the payout hierarchy — aka liquidation stack.

As an option holder, you typically hold common stock, which is at the bottom of the stack. First, any debt gets repaid—banks, lenders, and convertible notes get paid before any equity holders see a dollar. Next come preferred shareholders, who have negotiated terms entitling them to be paid before common shareholders. Finally, if there’s anything left, common shareholders (including employees holding options) are paid.

To gauge whether your options are likely to be worth anything in an exit, you need to understand the company’s liquidation structure—which is usually spelled out in the COI. This determines how proceeds from a sale or liquidation are distributed among different stakeholders.

Key things to look for in the COI include the following:

Return Multiples: Do preferred shareholders get just their original investment back (e.g., 1x), or a multiple of it (e.g., 2x or 3x) before the common sees anything?

Seniority: Are some preferred share classes ranked higher than others in the liquidation order? Senior classes are paid out before junior ones.

Preference: What exactly are preferred shareholders entitled to in a liquidation event? This includes the amount they’re owed (typically tied to their original investment), when they get paid (ahead of common), and any special provisions like interest or accrued dividends. Understanding the preference helps estimate how much needs to be paid out before common shareholders receive anything.

Participation: Are preferred shares non-participating (investors choose between their preference or converting to common) or participating (investors get their preference and also share in the remaining proceeds)?

These features can dramatically affect how much, if anything, is left for common shareholders. For example, a 2x preference means preferred shareholders must receive twice their original investment before common gets paid. If the company exits for a modest amount, that could leave common shareholders—and option holders—with nothing.

Return Multiple and Seniority Example

Let’s run through an example of what a multiple of return and seniority to preferred shareholders would look like in a COI – from Globus Medical in 2012:

Here, the holders of Series E Preferred Stock were entitled to be paid first in a liquidation event (even before the other series of preferred stock), and if that happened prior to January 31, 2009, then they would get 1.5 times their PPS.

Preference and Participation

In a liquidity event, preferred stockholders generally have two options:

Take their liquidation preference (e.g., get paid back their investment or a multiple of it), or

Convert to common stock and share in the remaining proceeds pro rata with common shareholders—if this results in a higher return.

This flexibility ensures preferred shareholders always take the better deal, which often leaves less value for common shareholders. 1x non-participating preferred stock is the most common structure, granting investors the right to either receive their initial investment back (1x) or convert to common stock to share in the remaining proceeds—whichever results in a higher return to them.

In some cases, preferred stock can even be participating, meaning holders not only get their preference first but also share pro rata in the remaining proceeds with common shareholders. While this structure is less common, it does still happen (particularly in later rounds)—and it’s especially important to look out for.

You can often find these terms in the company’s COI. By reviewing the number of authorized shares and the liquidation preferences tied to each class of preferred stock, you can do some rough calculations to estimate how much each series of preferred stock would be paid before common shareholders receive anything.

Note, it’s not a perfect calculation as there usually are more authorized shares than outstanding shares.

Example: Uniswap 2022

Let’s look at a real-world example of 1x non-participating preferred – from Uniswap in 2022:

The above tells us the authorized number of shares, including each series of preferred stock.

Above tells us this is 1x non-participating preferred: the preferred get paid first (preference) — i.e. they get 1 times (1x) their original investment if there isn’t enough to go to everyone. If there is enough for the common and preferred, then the preferred convert into common and share in those proceeds (participation) pro rata with the other shareholders.

Here, we can see the PPS (i.e. original issue price) of the Seed and Series A.

Now — using the information from the COI, let’s figure out how much preferred stock must be repaid before common shareholders receive any proceeds in a liquidation event. By multiplying the number of authorized shares for each preferred series by their respective PPS, we can estimate the total liquidation preference amount that takes precedence over common equity:

The total preference for preferred shareholders was around $12.7 million.

This means that, in a liquidation event, $12.7M would need be distributed to preferred shareholders first, before any money flows to common shareholders—not including any debt that might come before all equity holders. Huh…interesting…

Again, these are approximate estimates to provide a general sense of the figures involved, not precise calculations.

Why? The number of authorized shares does not necessarily equal the number of outstanding shares. Companies often authorize slightly more shares than they immediately issue, typically maintaining a 3–5% buffer in the latest series of preferred stock. This buffer provides flexibility for future needs, such as issuing stock warrants in connection with bank loans.

3. Ask the company what percentage of the fully-diluted shares your options package represents

In addition to understanding the potential value of your option package and where you fall in the liquidation stack, it’s also helpful to ask what percentage of the company’s fully-diluted cap table your grant represents—essentially, how much of the pie you’re being offered. This gives you another lens to evaluate your equity: not just what it might be worth someday, but how much ownership you’re actually being granted relative to the whole company at the time of grant.

You may be able to find some metrics around what’s a typical percentage of the fully-diluted for someone at that role and level in another company. You can then ask around to peers or perhaps gleam some numbers on Reddit. There are also paid, firewalled metrics you can pay for if so inclined or if you have a friend in HR.

Thinking about your options package as a percentage of the cap table can be a helpful, complimentary way to evaluate its value. Note that as a company grows and their cap table increases, those percentages will likely go down over time.

F. Beware of Companies that Don’t Look Out for Employees

Anecdotally, you’ll hear about companies making decisions that hurt employees’ options under the catchall in the stock plan – that the company can basically do whatever it wants (recall above that the company can substitute or cancel options or stock under the stock plan without any compensation to you). Usually, under a merger:

Vested options are cashed out or converted into shares of the acquirer.

Unvested options could be accelerated (vested immediately), replaced with new unvested options in the acquirer, cashed out, or cancelled entirely.

Suffice it to say, everything depends on the deal. The company and board have ultimate leeway to make the “best decision” for shareholders.

A 2021 study from ASU reveals that in about 80% of mergers and acquisitions (M&As), employee stock options are often modified or canceled to reduce company costs, benefiting shareholders instead of employees. The study, which examined 1,277 deals between 2006 and 2014, found that canceling stock options could reduce the value of employee compensation by an average of 38.4%, leading to a 3-4% increase in market value for the target companies. While this cost-cutting benefits shareholders, particularly in cases where employee losses are high, it can negatively affect employees who lose potential future gains from their stock options.

You should monitor what is going on at your company or risk being left behind. Below are a few examples of companies who were willing to throw employees under the bus:

In 2011, Skype, under Silver Lake's ownership, fired executives before its sale to Microsoft to avoid paying out their vested options, using complex legal clauses to invalidate them. Link

In 2017, Juno, a ride-hailing company, was acquired by Gett for $200 million, but cancelled its restricted stock unit program for drivers instead offering cash bonuses. Link

Most recently, OpenAI threatened to take back stock options from former employees if they didn't sign a non-disclosure agreement. The company has since apologized and promised not to do this in the future. Link

You can see why negotiating acceleration is so important because it can protect against these types of incidents.

G. Action Items - What Should I Ask For?

Now that you understand how the sausage is made, hopefully that empowers you to stand up for your own interests. If you don’t ask, you don’t get. It is harder to negotiate for more compensation once you start working for a company. It’s easier at this point, since the company wants to land you. Ask these questions to evaluate your option plan and what you should negotiate for:

Can I get a copy of the stock plan/form of option grant and most recent certificate of incorporation? If I can’t get it until after I onboard, can you walk me through the key terms?

What is the vesting schedule?

Can I get an early exercise option?

When do the options expire?

What happens if I leave the company?

What are the acceleration terms of my shares?

What’s the 409A? When was it? Is the strike price of my option the current 409A value?

What percentage of the fully-diluted shares are my shares?

Are there any transfer restrictions?

What’s the company’s discretion to cancel shares and options?

Does the company have employees sign a non-disclosure agreement when they leave?

Take the time to understand what you’re being offered and seek professional advice if needed. Your equity could be worth a significant amount in the future, but it’s essential to ensure that you’re protected and that the terms are favorable. It may be worth paying a lawyer and/or accountant to help you assess your options (pun intended) to avoid long-term bigger dollar value pains.

[Special thanks to Chris Ahsing, Bryan Edelman, Naveen Pai, Sam Silverberg, and Zack Skelly for their review.]

Images:All original images are AI-generated with using a combination of Dall-E, Firefly, DreamStudio and Pixlr.

Disclaimer: This post is for general information purposes only. It does not constitute legal advice. This post reflects the current opinions of the author(s). The opinions reflected herein are subject to change without being updated.